Generative AI bear Gary Marcus called the AI capex boom the “greatest capital misallocation in history.” Goldman Sachs analyst Eric Sheridan reaches the opposite conclusion in his “AI in a Bubble?” research package. Sheridan argues that this is not a hope-and-hype cycle like 1999 but a scale and monetization cycle, with tangible revenue growth and extraordinary market momentum.

So, who’s right? Jobs, pensions, and trillions of stock-market dollars, are at stake with implications for all of us.

I focus on Amazon Web Services (AWS) as the most informative window into the broader conundrum: it is the largest of the cloud businesses, the one with the cleanest revenue disclosure, and the one whose CEO has put the most specific quantitative defense on the table.

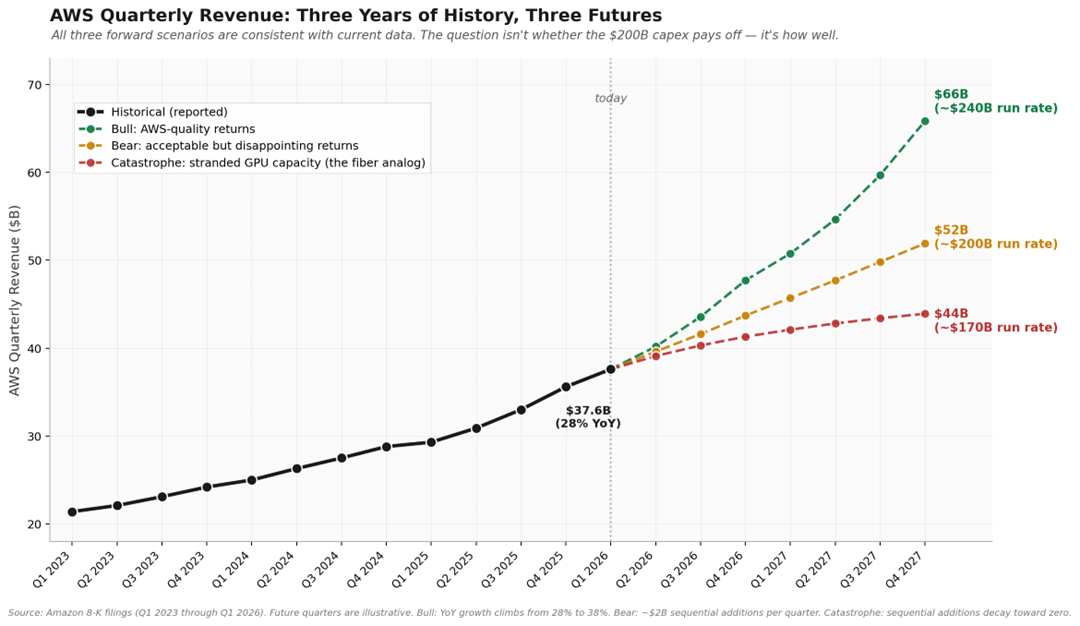

The chart below previews where this analysis lands: three plausible curves for AWS revenue, all consistent with the data through Q1 2026, each implying a different return on the $200 billion Amazon plans to spend this year. The disagreement between bulls and bears is essentially a disagreement about which curve materializes.

The bulls argue that hyperscalers fund this build-out from cash flow rather than debt, which makes the AI capex boom different from the historical telecom and railway bubbles. Indeed, AWS grew 28% last quarter, its fastest pace in 15 quarters, validating that enterprise demand for AI compute is real and accelerating.

Amazon CEO Andy Jassy has framed the company’s $200 billion 2026 capex plan as demand-driven rather than speculative, with strong expected return on invested capital. Stanford professor Gilad Allon offers the strongest non-Wall-Street version of the same argument: the AI build-out is funded primarily by cash-rich incumbents rather than leveraged speculative entrants, and high barriers to entry in chips, data centers, and power limit the kind of fragmented overbuilding that produces classic bullwhip dynamics. In essence, the bull case is that the technology is real, the demand is real, and being too cautious is its own kind of mistake.

In contrast, the bears argue that the AI capex math depends on assumptions that current operating numbers don’t yet support.

Venture capitalist Tom Tunguz notes that Bank of America projects hyperscaler debt issuance of $175 billion this year, six times the prior five-year average — a sharp departure from the cash-flow-funded story the bulls rely on. The asset-durability defense runs into Microsoft’s own admission that $37.5 billion of a single quarter’s capex was allocated to short-lived assets, mainly GPUs that depreciate in five years rather than the thirty-year horizon of telecom or rail.

Beyond the curve question, the bears point to financial fragilities that run independently of demand: Oracle’s leverage, Amazon’s sharp pivot to debt funding, and the circular customer-financing arrangements that tie hyperscaler revenue to a small number of model labs whose own revenue depends on capital markets staying open. In essence, the bear case is that the financial structure is changing, the demand assumptions are fragile, and being too aggressive is courting financial disaster.

Returning to our chart, the structure of the disagreement becomes concrete. The bull case assumes that the recent acceleration in AWS growth is the new normal and that growth rates keep climbing — producing roughly $66 billion in quarterly revenue by Q4 2027 and AWS-quality returns on the $200 billion capex.

The bear case assumes the recent acceleration was a catch-up move and that sequential dollar additions stabilize around the current $2 billion per quarter — producing roughly $52 billion in quarterly revenue and acceptable but disappointing returns.

The catastrophe case is below the bear case: AI workload demand actually reverses, and the GPU layer no longer earns enough revenue to recover its cost. The gap between the bull and bear cases is not whether the capex pays off but how well it does.

Consider the late-1990s fiber boom, when telecom companies laid more than 80 million miles of fiber-optic cable across the U.S. to carry the data traffic of the emerging internet. It didn’t collapse because operators ran out of money. It collapsed because WorldCom told the market that internet traffic was doubling every hundred days when the actual rate was once a year. The predicted curve was wildly off, and capital flowed accordingly.

By 2002, 85 to 95% of the fiber laid in the 1990s remained dark, and roughly $2 trillion dollars in market value had been wiped out. Demand eventually arrived — YouTube, streaming, the cloud — but it arrived a decade later, and the people who built it out lost their shirts. The relevant question for AI is not whether demand exists, which it plainly does, but whether it is growing fast enough to absorb $700 billion in annual capex

The data that resolves the disagreement is roughly 12 months away and will arrive in the regular cadence of quarterly earnings. By Q1 2027, the divergence between the bull and bear paths becomes visible in the AWS data: at that point, AWS quarterly revenue will be either accelerating toward the high $40 billions, tracking flat against the low $40 billions, or showing the first signs of inflecting downward.

None of those outcomes is currently disprovable from the trajectory through Q1 2026, which is why the hyperscalers can keep raising debt and the market keeps buying it. Anyone telling you they are certain which curve will materialize is selling something.

As for me, I just bought a 12-month supply of popcorn.

[Editor’s note: GeekWire publishes guest opinion pieces representing a range of perspectives. The views expressed are those of the author.]

Read the full article here